Prosperity continues in 2017, but the cycle is heading toward a fall

The upward momentum that commercial real estate prices and values have been experiencing has recently slowed relative to their appreciation trajectory since their amazing recovery starting two years after the credit crisis. Given the challenges in today’s world and the many dynamics affecting commercial real estate, the economy, and the financial markets, it is time to fully understand the next phase of the current market cycle.

As the transition moves to this next phase, it is time to examine the key forces that will dictate one of the following:

- market adjustment;

- market correction; or

- major market correction or crisis.

All investors, including commercial real estate investors, are focused on when is the end of this phase of the cycle; what will be the triggers that push the industry into the new era; and what should commercial real estate professionals expect for value and price changes.

Final Innings

Looking back, commercial real estate has been a stellar investment performer and a preferred asset class since shortly after the credit crisis. This continues as institutional investors consider commercial real estate as the top investment alternative.

It is a real asset, offers strong income, and has matured as an asset class. As shown in Exhibit 1, the strength of this confidence in commercial real estate and stocks has declined from peak levels of a few years ago, while investor confidence in cash has grown and confidence in bonds remains relatively low. This pattern signals that a market turn is around the corner but not how far out.

Commercial real estate looks like the best investment choice, and the rationale stills holds true. Investor focus must be in preparing for the next phase and determining when it will turn.

Situs RERC recently polled real estate professionals at the 10th annual University of Chicago Booth School of Business Real Estate Conference about where the industry is in the current cycle. Using a baseball analogy to compare the results of this real time poll and Situs RERC’s view, commercial real estate is in the bottom of the eighth inning at the end of 2016 and will enter the ninth inning in 2017.

The year 2017 is expected to be much like 2016, with commercial real estate prices and values on average increasing sluggishly and cap rate compressionstalling. Like the final game of the 2016 World Series, the industry will go into extra endings due to the influences and forces that evolved since the Great Recession and through the transition into the next era. At some point, the extra innings will end and the game will be over. Just as in baseball, it is difficult to tell how many extra innings will be played to usher in the next phase of the cycle.

If this is the case, examination of the final script and the players that will deliver that conclusion. In the commercial real estate investment game, other influences and forces will determine the end of this stellar performance.

Rising Risks

Looking to 2017 and beyond, the risk factors facing the economy, the investment environment, and commercial real estate are considerable. The Federal Reserve has clearly called the plays and influenced the key aspects of the economy, interest rates, and financial markets. The Fed’s future decisions will also influence the next cycle, as its members will have to eventually increase short-term interest rates.

In a surprising turn of events that stymied the pollsters, Donald J. Trump was elected president. After a campaign fraught with acrimonious rhetoric, the president-elect’s tone and tenor has changed. Although the election brings uncertainty, this uncertainty appears to be positive for investment, at least for now.

Typically, what is good for the economy is good for commercial real estate. Mr. Trump’s proposed pro-growth fiscal policies, however, have stoked inflation worries, sending Treasury rates upward.

The cap rate compression during the past few years has been driven by a low interest rate environment. If interest rates rise too quickly, commercial real estate may not be able to absorb the impact. Only time will tell whether President Trump’s policies come to pass, but since commercial real estate tends to lag economic trends by at least six months, commercial real estate growth in 2017 will likely hold steady.

Also, potential black swan events could lead to a major market correction. Although it is tempting to believe there is a nice script of events that will happen in sequence smoothly and predictably during this next cycle, not everything goes as planned. This is true especially since the new set of players has not experienced these kinds of events since the Great Recession.

It is all new and the economy will reach anormalized level, but there will be ups and downs. The question is, how volatile will the transition be for commercial real estate?

Most important for the industry is the reality that the Fed will raise short-term interest rates several times throughout 2017. The primary driver of low long-term interest rates has been the Fed’s low rates, a sluggish economy, and low inflation. Commercial real estate investment lives on debt to the tune of 50 percent or higher and remains one of the most leveraged asset classes.

As a result, the industry has been one of the biggest beneficiaries of this historical low interest rate environment that has pushed cap rate compression to a new level. Now the Fed is playing the waiting game with rate hikes since economic conditions have continued to improve. Situs RERC’s expectation is that a series of interest rate increases is on the horizon.

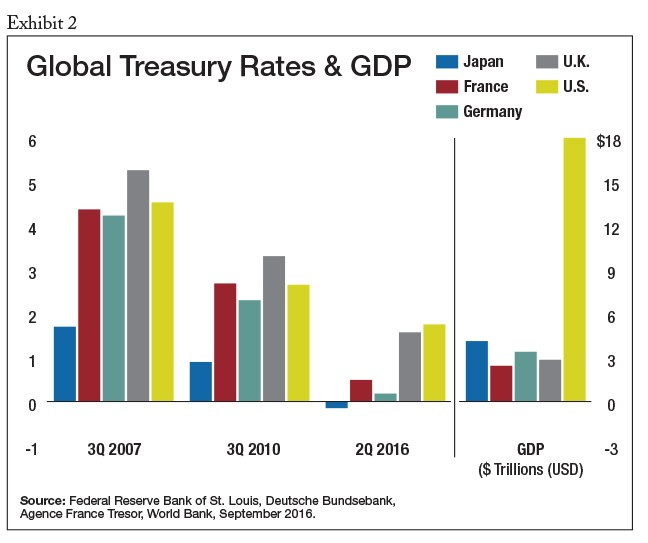

Although it is likely that the Fed will continue to raise interest rates in 2017, rates are still at historical lows for the major global economies (see Exhibit 2). While central banks are trying to fight their country’s respective economic problems, the negative impact of this uncertainty is felt in the U.S. In fact, the Federal Open Market Committee hesitated to raise rates in 2016 in part due to unanswered questions of global growth amid speculation about the impact of Brexit.

Situs RERC’s view and that of its investment survey respondents varied as to when 10-year Treasuries were expected to normalize. Although some respondents felt that Treasuries would normalize during the next one to three years, the majority thought it would be three to five years.

In addition, respondents believed 10-year Treasuries would normalize at a level of 3 percent to 4 percent. With current rates at below 2 percent, the U.S. economy has baked this level into the prices and values of commercial real estate.

Long-term rates are going to look OK in the future relative to past levels, but they will increase by 50 to 100 percent from today’s level. This means that cap rates and discount rates will have to respond. The commercial real estate rate response will not be a simple answer.

Steady ROI

While the economy continues to crawl, annual commercial real estate income returns have been a positive note in an environment filled with uncertainty. Income return has been relatively stable during the past decade with the most recent quarters resulting in rolling annual returns of 4 to 6 percent, which is approximately double the dividend yield seen in the S&P 500 over recent quarters.

According to the most recent Situs RERC institutional investor survey data, expected rents have remained stable or increased for most of the major property types compared to a year ago with the exception of the suburban office, retail power center, and regional retail mall property types. Because of long-term leases already in place, investors can expect stable rent payments in 2017.

The spread between real estate returns and 10-year Treasuries has been around 550 basis points to 600 basis points during recent quarters. The solid spread between real estate returns and 10-year Treasuries is indicative of the current market environment, with low interest rates maintaining the spread. The spread for real estate is greater than the spread of corporate bonds compared to 10-year Treasuries.

Considering the level of risk, the spreads indicate that real estate provides a solid risk-adjusted return compared to alternative fixed income investments and has the capacity to take on some of the interest rate hikes of the future but not all of the likely interest rates moves.

Differentiating Sector Fortunes

According to Real Capital Analytics, transaction prices for all the major property types are as high or higher than they were prior to the market crash, which suggests the peak for commercial real estate pricing. However, prices are not the only consideration when assessing the worth of a property; price needs to be assessed in reference to the value of the property.

According to Situs RERC’s institutional investment survey respondents, investors believe overall commercial real estate values and prices are generally moving in tandem.

Respondents to the Situs RERC’s surveys rated the major property types on return on investment compared to risk. For overall commercial real estate, there was no change in third quarter 2016 from third quarter 2015, with respondents maintaining that return outweighed risks for investors.

Exhibit 3 shows the return vs. risk and value vs. price ratings before, during, and after the credit crisis. While current ratings reflect that commercial real estate return outweighs risks and these values are nearly equal to price, it is important to note that ratings have decreased compared to three years ago and are trending toward levels similar to those before the Great Recession. These results hint that a market correction is near.

Changing Markets Landscape

Situs RERC monitors 48 metros that are split into primary, secondary, and tertiary markets based on the statistical distribution of value and price metrics. The best opportunities in each of these markets were based upon the lasting, sustainable value characteristics of the individual metros compared to their pricing levels.

Primary markets are typically preferred by big investors because of the perceived durability of the market when things get tough for commercial real estate. These cities offer a better risk-adjusted return over the long run due to its long-term establishment and economic diversity.

However, prices in these areas, particularly for Class A properties, are at record highs. Due to increased foreign capital, solid property fundamentals, and scarce supply, costs are likely to continue to increase for the primary markets into 2017. Investors who are yearning for higher yields or are chasing alpha may want to look to core-plus opportunities or spread their wings and venture into new markets, however.

Dallas and Seattle ranked No. 1 and No. 2, respectively, with regards to value vs. price investment opportunities for the industrial, office, and multifamily sectors.

Extreme competition in primary markets, particularly for Class A properties, is driving investors toward secondary and tertiary markets where higher yields can be found. At the same time, the risks associated with the secondary markets have been tempered by strong population growth and improving economies.

Austin, Texas, tops Situs RERC’s list as the best secondary market in which to invest, particularly for office properties. Austin had the largest population growth of all the secondary-metros measured by Situs RERC, and that population is forecasted to continue to grow in 2017 and its employment rate outpaces national levels. Yet, pricing in the Austin market is still reasonable, helping to make Austin the No. 1 secondary market.

For tertiary markets, Omaha, Neb., takes the No. 1 spot in the office, retail and multifamily sectors among the tertiary markets. Strong fundamentals and relatively solid pricing contribute to its high ranking.

The retail sector, buoyed by wage growth and strong auto sales is a particular bright spot for Omaha’s market. Transaction volume in the office, retail and apartment sectors has increased in 2016, including a couple of high-profile deals. This activity is leading to an uptick in prices compared to the previous quarter.

Future Challenges

In revisiting the original concerns, most professionals responding to Situs RERC’s various surveys believed a market correction will not occur until about 2019, with the market correction expected to range from 15 to 20 percent. While the end of this cycle is on the horizon for commercial real estate, the market appears poised to offer relative solid income returns in 2017 and modest to flat appreciation.

Although commercial real estate prices have increased tremendously since the Great Recession, prices alone can mask the true returns investors can expect. Situs RERC used statistical modeling to forecast those values during the next several years.

When considering commercial real estate from a capital return perspective only, the increase in its values are not as dramatic as prices, given that most of the run-up in values are driven by capital expenditures.

As shown in Exhibit 3, the commercial real estate value index declined 32.1 percent in the early 1990s. The subsequent recovery spanned over a decade as the value index grew by 73.2 percent. However, the industry’s value index dropped 31.7 percent in the wake of the Great Recession.

Today, values have increased 49.9 percent, which is 20.3 percent higher than in the 1990s. Situs RERC’s outlook for commercial real estate values over the next several quarters wanes slightly until growth becomes negative by the end of 2017.

Situs RERC predicts that commercial real estate will continue to be the best asset choice in 2017 and most likely for several years to come compared to stocks and bonds. It is difficult to predict when the next market decline will occur, but there is overwhelming evidence that interest rates will increase in 2017, although slowly. As the industry progresses beyond 2017, more unknowns enter the equation and prognostications become increasingly hard to make.

For example, if the Fed raises interest rates too much or too suddenly, higher-than-expected inflation may occur in 2018 and beyond. In addition, major geopolitical events and shifts in foreign and domestic economies could bring an end to the long streak of prosperity for the industry.

There is a market correction on the way estimated to be approximately 20 percent, and this will start appearing at the end of 2018 or the beginning of 2019. The market correction will play out over the next two years, and challenges and bumps will occur along the way.

Commercial real estate is in the best position among the alternatives to manage through the next phase if supply stays in check and if crazy debt stays out of the game.