The robust development pipeline has not dampened investor appetite.

The multifamily housing sector is defying gravity. Property fundamentals and investor appetite are holding steady under a heavy load of new deliveries.

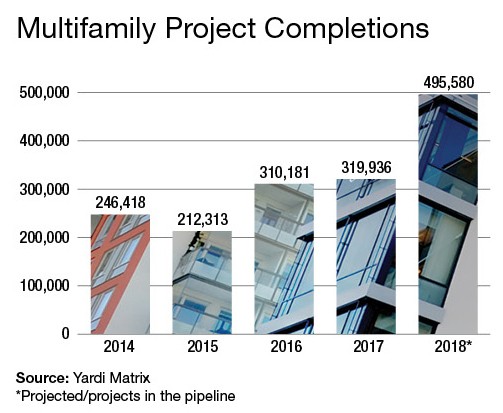

The multifamily market already is several years into its bull run, generating strong property performance and a surge in supply. Yet renters continue to absorb much of the new inventory coming onto market, with national vacancies rising only 10 basis points in the second quarter of 2018 to a 4.7 percent average, according to Yardi Matrix.

“We see the U.S. multifamily market as being dynamic, especially over the past year,” says Doug Ressler, director of business intelligence at Yardi Matrix in Santa Barbara, Calif. Approximately 875,000 new units were completed between 2014 and 2017, with another 140,000 units in the first half of 2018. Most construction occurred in the top 30 metro areas, with a high concentration of class A luxury apartments being built.

Some markets are showing softening in the high-end segment of the market, especially in the Midwest. Yardi Matrix is predicting that overall performance is going to be fairly consistent and positive in most cities, Ressler notes. In fact, high-growth metros such as Dallas; Charlotte, N.C.; Nashville, Tenn.; and Denver all saw an improvement in their occupancy rates during the first half of 2018, with vacancies in all four markets hovering at around 5 percent. “With deliveries in their third year of cycle peaks, the increase in occupancy rates demonstrates the resilience of apartment demand,” he says.

The big question is how metrics will hold up, especially with a significant number of projects still underway or planned. “Development remains strong in all sectors and all submarkets here in Denver,” says Rick Egitto, CCIM, principal of capital markets in Avison Young’s Denver office. “Vacancies have ticked up a bit to just over 5 percent, but given the large amount of product delivered, this is not significant,” he says.

Yet the players have changed in terms of who is actively building. Some early groups constructing apartments in Denver in 2010 to 2013 have slowed their activity, while other national firms have stepped in to pick up the slack, Egitto says. Developers also are less active in the core of the city and now are taking a bigger step into suburban markets, such as Aurora, Parker, and Golden, to find new opportunities.

Rising Costs Create Added Pressure

Developers recognize the impact of rising construction costs and moderating rent growth. Although there has been a slight pullback in units under construction, the pipeline of prospective projects actually is climbing, Ressler notes. “We think those challenges are going to play to the larger, established industry veterans,” he says.

Developers are being more selective in where they build, too. Development is continuing in gateway markets and metros that are dense enough to handle large fluctuations in supply. Conditions also remain favorable in secondary markets that are leading the nation in employment growth or where population growth is driving demand, including key markets in Florida and the Southwest, Ressler says. Areas with strong growth potential, like Austin, Texas; Charlotte, N.C.; and Miami, and strong secondary and tertiary markets with good economic drivers, such as a growing technology hub like Boise, are attracting developers as well, he says.

Decatur, Ga., is a tertiary market where rents are “going through the roof” due to new construction that is delivering at higher price points, according to Jim Brewer, CCIM, broker and owner of Decatur-based Brewer Agency LLC. “I have never seen this much new construction in this small a market in my life,” he says. Decatur started working on a pedestrian-oriented community about 30 years ago that’s now in full blossom, attracting young, upwardly mobile renters, he adds.

Construction costs are perhaps the most significant headwind developers are facing. In some cases, costs for materials and labor have risen nearly 30 percent in the past 18 months.

Rising construction costs are “squeezing the juice out of the yield” on development, says William A. Shopoff, CCIM, president and CEO of Shopoff Realty Investments, an apartment developer and investor in Irvine, Calif. Construction costs have moved at a multiple of inflation over the last two years, while rent growth in many markets has been slowing. “We are seeing developers show a higher degree of caution and approaching their underwriting for future deals with a little less optimism,” Shopoff says.

Rising interest rates and higher construction costs are putting more pressure on land prices and making it more difficult to make the numbers work on new projects. “Construction costs have risen significantly in Denver, and it has really caused the market to adjust to the new rents that have to be obtained,” Egitto says. For example, it is not unusual to see urban rents in the $2.50 to $3 per-square-foot range, and some unique locations approach $4 psf, while suburban projects generally can work at a lower $2 psf rent, he says.

In some cases, developers have built projects in Denver with an expectation that they can collect the higher rents, and they have continued to see projects lease up quickly even with these higher rates, Egitto says. Part of the success is due to the significantly different amenities compared to the older product, even though existing price comps might not have supported that price point, he says.

Investors Vie for Value-Add Deals

Investors still have a huge appetite for value-add acquisitions, even as buying opportunities have become increasingly difficult to find. “We think the value-add market is extremely competitive,” Shopoff says. Although the firm works on value-add projects nationally, it’s been more than a year since the company has taken on any new projects of this type. “Markets cycle, and there will be opportunities again, and we are always looking. But right now the yields we can achieve on value-add you can find in a better arena,” he says. Instead, Shopoff has redeployed its capital to focus on development projects, as well as pre-development projects where it buys and entitles land for multifamily and then sells to other developers.

With value-add deals getting picked over in the gateway markets and largest secondary markets, investors are looking at smaller secondary and even tertiary markets. “We have a tremendous amount of interest from investors nationally and internationally for value-add deals in the Louisville market,” says Tyler Chesser, CCIM, vice president of commercial real estate investments at Gant Hill & Associates in Louisville. “We have gotten to a point where those deals are fewer and farther between than they were a few years ago, but opportunities do still exist,” he adds.

Competition has motivated some investors to embark on value-add 2.0 projects, essentially taking a property that already has undergone some improvements and going back in for a second round of more in-depth renovation. “We have gotten to a point where most investors who are capturing opportunities are very savvy,” Chesser says. Some of these veteran value-add investors can readily identify repositioning opportunities that others don’t recognize. They are comfortable paying very aggressive prices because they see the potential to add more amenities or reduce the expense load on the operating side, he says.

For example, Chesser recently represented the buyer in the purchase of the 83-unit Lofts of Broadway in Louisville for $6.8 million. The Downtown Louisville warehouse was converted to loft-style apartments in 2005. In this case, the buyer sees an opportunity to further upgrade units with additions such as granite countertops and add new on-site amenities. “We believe that this is going to be an incredibly successful project because of the demand for this type of product,” Chesser says.

Investors Still Favor Apartments

New supply has not put a damper on investment sales transactions. Multifamily sales volume reached $69.8 billion in the first half of the year, up 11.5 percent year-over-year compared to the $62.6 billion in properties that traded during the same period of 2017, according to Real Capital Analytics.

Many capital investors still in the market are interested in multifamily buildings, especially those who plan to hold assets for the long term. Yet investors are keeping close tabs on supply growth, decelerating rents, and interest rates in what most agree is a mature stage of a prolonged growth cycle. Many investors are being selective in what and where they are buying, and some metros are still seeing a big gap between buyer and seller expectations, which is slowing transactions.

“Caution is being exercised by most to ensure past mistakes of a previous cycle are not repeated,” Chesser says. In Louisville, investors are concerned about oversupply and slowing rent growth, and the current lease up and stabilization of new communities are being monitored closely. However, the reports of outpaced performance to expectations continue to fuel demand in the Louisville market, especially among national and international buyers looking to achieve higher yields than they can find in some gateway markets and larger secondaries. “We have found that our market has really struck a chord with investors. We have yield and a diverse market with employment across many different industries, population growth, and many strong indicators that folks like,” Chesser says.

Other markets have seen a notable shift. Buyer sentiment has changed radically in New Jersey’s Gold Coast market over the past six months, along with higher interest rates, while seller expectations have not changed. That disconnect is causing stagnation in the market, says Chris Cervelli, CCIM, president of Cervelli Real Estate & Property Management in North Bergen, N.J. “Properties are starting to sit around a little bit longer,” he says. Investors are not oblivious to headwinds such as rising interest rates, slowing rent growth, and a still-active development cycle. In addition, the trade wars and tariffs are making some investors nervous. “Everybody feels like the music is stopping, and no one wants to be left holding that bag when it does,” he says.

The flip side is the abundant debt and equity in the market, and many investors and lenders like the risk-adjusted returns on multifamily units relative to investment alternatives.

“There is still a tremendous amount of equity – both institutional and private equity – that loves the multifamily space,” Shopoff says. “If good product comes on the market, there are multiple buyers for it.” Interest rates have moved higher, but rates are still relatively low. People can still buy a property at a 5 percent cap rate, put debt on it at 4.5 percent, and have positive leverage and rent growth, plus some tax shelter and inflation protection, he says. “I don’t think there’s any shortage of buyers today. That shine could come off at some point, but we don’t see it,” he adds.

Creative Developers Battle Rising Costs

by Beth Mattson-Teig

Developers facing the dual pressure of rising construction costs and slowing rent growth are finding creative ways to make the numbers pencil out on new projects.

Higher construction costs are putting more pressure on land prices. Developers also are exploring other alternatives to maintain yields, such as increasing density or value-engineering projects. Some developers are offsetting higher construction costs by offering micro-units that allow the developer to deliver units at a more affordable rate, while still capturing a higher rent per square foot.

In Denver, for example, a former hotel adjacent to Mile High Stadium was converted into the Turntable Studios, a micro-apartment project with 179 units that range from 330 to about 800 sf. “I also think the investor market finds those micro-units attractive. The one or two that have sold here have generated very high per door prices,” says Rick Egitto, CCIM, principal of capital markets in Avison Young’s Denver office. “Renters like it, and investors like it as well,” he says.

A few innovation leaders are leveraging new design, engineering, and building systems and processes to reduce construction costs. “There are people who think they have a better mousetrap,” says William A. Shopoff, CCIM, president and CEO of Shopoff Realty Investments, an apartment developer and investor in Irvine, Calif. “We’re not quite there yet, but we do think that we’re going to see some technological changes in construction that are going to drive value,” he says. Some developers are using various levels of prefab with modular or factory-built units that are assembled on site.

Denver-based iUnit currently is designing factory-created, prefab units that are assembled on site. The company built the 40-unit Elliot Flats in the Lower Highlands area of Denver and has a second project underway. Both projects also adhere to sustainable building practices with an aim to achieve net-zero energy efficiency.

Menlo Park, Calif.-based design and construction firm Katerra works to squeeze efficiencies across each step of the building process — from its design, technically engineered materials, supply chain, and construction. Its strategies range from more cost-effective product sourcing to off-site manufacturing that provides greater precision, higher productivity, and more quality control.

In a rising cost environment, these cost-effective building solutions could help developers and investors preserve yields and address the bigger issue of creating more affordable housing as well. If developers can build apartments cheaper, that alone is a big advantage. If they can build apartments both cheaper and faster, that’s a huge advantage in a competitive marketplace. “You not only save interest expense, but you start generating revenue faster — and more importantly you know what market you’re delivering into,” Shopoff says.

Since most urban projects take 24 months to complete, builders end up delivering projects in a different market than they started in terms of competition, rents, and economic drivers. For developers that can build an apartment building in six to 12 months versus 24 months, and at a cost savings of 5 to 10 percent, that’s a huge competitive advantage, Shopoff says. No developer wants to be on the wrong side of the curve.

Investing in Today’s Multifamily Market

by Barry Saywitz

Investors are facing many challenges in the multifamily market. With the housing market on an upward slope, home prices rising, and interest rates ticking up, homeownership is more difficult to achieve. In addition, baby boomers are selling their homes for retirement money without purchasing new ones, and millennials prefer renting. The resulting rental market demand continues to push multifamily rents to an all-time high. This increase in rents drives values for multifamily properties, making them an extremely desirable investment vehicle.

The limited number of quality properties for sale and significant amount of available capital means that buyers are chasing every deal. The average sale time of a property has decreased dramatically, and the terms of the transaction and the time frames for the buyer to perform have increased. It’s a seller’s market — and the buyer assumes several risks.

Financing a property with a cap rate lower than the interest rate is difficult, unless there is significant upside in rents. Smart investors need to evaluate whether they should raise rents nominally, which would avoid pushback from existing tenants, or raise rents significantly, which means investing capital and remodeling the property.

When a buyer remodels or raises rents, it adds downtime from turnover, which must be accounted for in the overall return. While investors who acquired properties in the last few years locked in extremely low interest rates, these rates are on the rise. As a result, mortgages will increase in the coming years when these loans roll from fixed rate to adjustable or reset at the future rate. If rents do not increase at the same pace, investors will see diminished returns.

Many experts believe that we are in the ninth inning of this nine-inning real estate cycle. Those currently investing may be overpaying and in serious danger of a market adjustment or interest rate increase, both of which would negatively affect the overall return and value of the property.

Money still can be made in the multifamily market. Many properties have significant upside in rents, and there are ample opportunities for the savvy and careful investor. But those who believe they are going to buy property and sell in a few years to make a profit need to be wary of interest rates and rent growth. In addition, if the market should flatten or turn, these investors and property owners will be in significant trouble.

Investors with a sound investment strategy will be successful in both the short term and the long term.

Barry Saywitz is president of The Saywitz Co., a national commercial real estate brokerage, investment, consulting, and management company in Newport Beach, Calif. Contact him at bsaywitz@saywitz.com.